You walk into the pharmacy, hand over your prescription for a life-saving medication, and watch the total on the screen climb past $400. You expected a $20 copay. This isn't just a bad day; it's a coverage gap you missed during enrollment. According to recent data from Georgetown University cited by HealthPartners, nearly two-thirds of all adults in the United States rely on prescription drugs. Yet, 63% of people shopping for health plans fail to check if their specific medications are covered until after they've already signed up. The result? A quarter of those shoppers end up changing plans the very next year because the costs became unmanageable.

Prescription drug insurance coverage is not a one-size-fits-all benefit. While 99% of Marketplace plans include this coverage as required by the Affordable Care Act, the details vary wildly between insurers. Some plans cap your insulin at $35 a month, while others might charge you coinsurance that adds up to thousands. Understanding the mechanics of your plan before you need a pill can save you more than just money-it can keep you adhering to your treatment plan. Here is exactly what you need to ask your insurance provider to avoid these costly surprises.

Is My Medication Actually on the Formulary?

The first and most critical question is simple: Does this plan cover my specific drug? Every insurance plan maintains a list of covered medications called a formulary, which is a categorized list of prescription drugs covered by a health insurance plan. If your medication isn't on that list, you are paying 100% of the cost out of pocket. Do not assume that because a doctor prescribed it, your insurance will pay for it.

Formularies change every year. A drug that was covered last year might move to a higher tier or be dropped entirely. When comparing plans, use the insurer’s online tool to enter your medications by name or National Drug Code (NDC). For Medicare beneficiaries, the Medicare Plan Finder requires NDC codes for accurate comparisons. Spending just 20 minutes verifying your meds against the formulary can save an average of $1,147 annually, according to an Urban Institute study. If your drug is missing, ask if there is a therapeutic alternative-a different drug that treats the same condition-that is covered.

What Tier Is My Drug In, and What Does That Cost Me?

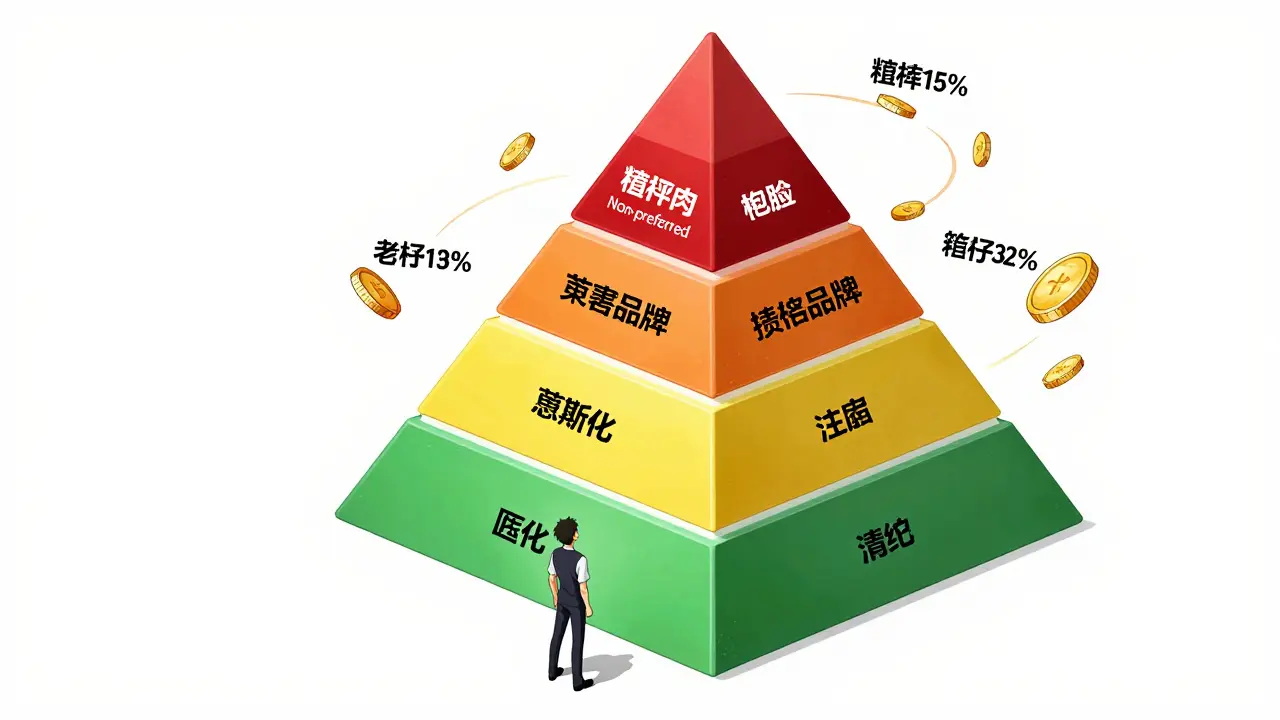

Once you confirm your drug is covered, you need to know its tier. Formularies are typically organized into four tiers, each with different cost-sharing requirements. This structure determines how much you pay at the pharmacy counter.

| Tier | Type of Drug | Average Copay/Cost |

|---|---|---|

| Tier 1 | Generic drugs | $10 copay |

| Tier 2 | Preferred brand-name | $40 copay |

| Tier 3 | Non-preferred brand-name | $100 copay |

| Tier 4 | Specialty drugs | 25-33% coinsurance ($1,000+ avg) |

If your medication is a generic, you’ll likely fall into Tier 1 with a low flat fee. But if you take a specialty drug-often used for complex conditions like cancer or rheumatoid arthritis-you could face Tier 4 pricing. Specialty drugs often require coinsurance, meaning you pay a percentage of the drug’s cost rather than a flat fee. With average out-of-pocket costs exceeding $1,000 per prescription for Tier 4, this distinction is vital. Ask your insurer: "Is my drug a preferred or non-preferred brand?" This single detail can swing your annual costs by hundreds of dollars.

How Much Do I Pay Before Coverage Kicks In?

Many people focus on the monthly premium but ignore the deductible. The deductible is the amount you must spend on healthcare services before your insurance starts sharing the cost. For prescription drugs, this matters immensely.

In the ACA Marketplace, Bronze plans have lower premiums but high deductibles, averaging $6,000. Gold plans have higher premiums but much lower deductibles, averaging $150. If you take regular maintenance medications, a Gold plan might actually cost you less overall despite the higher monthly bill. CMS modeling shows that someone filling 12 maintenance medications annually saves $1,842 with a Gold plan compared to a Bronze plan. Ask yourself: "Will I hit my deductible this year?" If you take daily meds, the answer is likely yes, making the deductible a key factor in choosing your plan.

Are There Restrictions Like Prior Authorization or Step Therapy?

Coverage doesn’t always mean immediate access. Insurers often use utilization management tools to control costs. Two common restrictions are prior authorization and step therapy.

- Prior Authorization: Your doctor must get permission from the insurer before they prescribe the drug. This is required for 28% of Medicare Part D prescriptions. It delays treatment and adds administrative hassle.

- Step Therapy: Also known as "fail first," this requires you to try cheaper, covered alternatives before the insurer will pay for the prescribed drug. This is used for 37% of Marketplace specialty drugs.

Ask your insurer: "Does my drug require prior authorization or step therapy?" If it does, talk to your doctor immediately. They may need to submit clinical justification to bypass these rules. Not knowing about these hurdles can lead to rejected claims and frustration at the pharmacy.

Which Pharmacies Are In-Network?

Your choice of pharmacy affects your price. Most plans limit coverage to specific networks. About 78% of Marketplace plans restrict coverage to certain pharmacies. Using an out-of-network pharmacy can increase your costs by 37% on average, according to the NAIC Consumer Report.

Check if your local pharmacy is in-network. If you travel frequently, ask about mail-order options for maintenance drugs. Many plans offer 90-day supplies via mail order at a discounted rate. However, for urgent needs, having a reliable in-network brick-and-mortar pharmacy nearby is crucial. Don’t assume your usual spot is covered; verify it directly with the plan.

How Does the Coverage Gap Affect Me?

For Medicare Part D beneficiaries, the "donut hole" or coverage gap is a phase where you pay a larger share of costs. In 2024, once your total drug costs hit $5,030, you entered the gap and paid 25% of costs until reaching $8,000. After that, catastrophic coverage kicked in.

However, the landscape is shifting. The Inflation Reduction Act introduced significant changes starting in 2025. The coverage gap is being eliminated, and there is now a hard cap of $2,000 on out-of-pocket costs for Part D beneficiaries. Monthly insulin costs are also capped at $35. If you are on Medicare, ask: "How does the new $2,000 out-of-pocket cap apply to my plan?" This protection prevents catastrophic spending on drugs, but understanding how your plan calculates toward that cap is still essential.

When Should I Ask These Questions?

Timing is everything. You cannot easily change your plan mid-year unless you qualify for a Special Enrollment Period due to a life event like marriage or job loss. Therefore, you must do this homework during open enrollment.

- Marketplace Plans: Open Enrollment runs from November 1 to January 15. Use the HealthCare.gov comparison tool to enter up to 15 medications and three pharmacies.

- Medicare: The Annual Election Period is October 15 to December 7. This is when you can switch between Part D plans or Medicare Advantage plans.

Don’t wait until January. Start checking formularies in October. If your current plan raises the tier of your medication or drops it entirely, you have a window to switch. Proactive verification is the only way to ensure your health insurance actually covers your health needs.

What should I do if my medication is not on the formulary?

First, ask your doctor if there is a therapeutic alternative that is covered. If no alternative works, you can request a formulary exception. Your doctor must provide clinical documentation proving why the excluded drug is medically necessary. The insurer may approve this exception, allowing them to cover the drug at a specific tier.

Is a Gold plan always better for prescription coverage?

Not always, but often for frequent users. Gold plans have higher premiums but lower deductibles and out-of-pocket maximums. If you take multiple maintenance medications, the lower deductible usually offsets the higher premium. Calculate your estimated annual drug costs against the plan’s deductible and copays to see which saves more.

How can I find the National Drug Code (NDC) for my medication?

The NDC is a unique identifier for every drug product. You can find it on your prescription bottle, in the patient information leaflet inside the box, or by searching the FDA’s National Drug Code directory online. Entering the NDC ensures you are checking the exact strength and manufacturer covered by your plan.

What is the difference between a copay and coinsurance?

A copay is a fixed dollar amount you pay per prescription (e.g., $20). Coinsurance is a percentage of the drug’s cost that you pay (e.g., 20%). Copays are predictable, while coinsurance costs can vary widely depending on the drug’s price. Specialty drugs often use coinsurance, which can lead to high bills.

Can I change my plan if my medication coverage changes mid-year?

Generally, no. You can only switch plans during Open Enrollment or a Special Enrollment Period triggered by qualifying life events. If your plan drops a drug unexpectedly, contact the insurer immediately to discuss exceptions or appeals. However, you cannot simply switch to a competitor’s plan without a qualifying event.